HMRC VAT Security Deposits for Struggling Companies

We have received a letter from HMRC and they have demanded a security deposit. What does that mean?

ReadHMRC VAT Security Deposits for Struggling Companies

We have received a letter from HMRC and they have demanded a security deposit. What does that mean?

ReadWhat is an HMRC Notice Of Enforcement?

Any creditor who is owed money has the power to serve a Notice of Enforcement if they obtain a court order. HMRC or landlords do not need a court order, however they must still obey strict regulations to retrieve debt.

Read

Company Bankruptcy Advice

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Managing Director of RMT KSA

Read

Is My Company Insolvent? The 3 Legal Tests & Director Duties

There are 3 tests to check to see if a company or business is insolvent. The cashflow test, balance sheet test and the legal action test.

Read

How to Save a Failing Business from Insolvency

A failing business is stressful for directors and its employees. Find out what the causes are and what can be done about it. Free advice

Read

CVA – What Is A Company Voluntary Arrangement?

A CVA or Company Voluntary Arrangement is a legally binding agreement with creditors allowing a a business to pay back a proportion of its debts over time

Read

What is Going Into Administration? A Guide for Directors And The Public

The content on this page has been written by Keith Steven and approved by Chris Ferguson Licensed Insolvency Practitioner and Director of RMT Recovery and Insolvency

Read

What is Balance Sheet Insolvency?

Balance sheet insolvency is when a company’s total liabilities outweigh its total assets. However, it may still be able to pay its liabilities when they are due.

Read

If My Company Goes Bust Will I Lose My House?

You will not lose your house if your company goes bust but if you have been guilty of defrauding creditors or have personally guaranteed company loans then it is possible.

ReadTime to Pay with HMRC

How Much Time Could I Get? This does depend on the circumstances. HMRC will usually agree that you can pay it back over 6-12 months. However, if you instruct a professional turnaround advisor, they can usually get longer, i.e., 2 years, as they have a working relationship with HMRC and will not put forward proposals by companies that would struggle to pay.So, if you can't pay Paye or VAT, then a Time to Pay Arrangement is an option. Time-to-Pay arrangements are made directly with HMRC. Take a look at their Business Payment Support Service to make sure you're choosing the right path. What are the criteria? Companies in debt to HMRC must apply to set up a Time to Pay Arrangement. HMRC will only accept a proposal if it is satisfied that you'll stick to the arrangement and repay all your taxes in full.It is your job to convince HMRC to allow you to pay your taxes over time by putting forward a reasonable proposal.Your proposals should be supported by evidence that these payments can be met, including:Forecasting sales Examples of how you can cut costs elsewhere A convincing argument proving your determination to pay your taxesIt is very important not to offer to pay back more than you can afford. If you do, then HMRC may reject the proposal, putting you in a worse situation. It's best to consult a financial or turnaround advisor to assess affordability levels.If accepted, HMRC will give your company a period of time to pay your taxes. This is usually between 6–12 months, but in some cases it can be longer. How do I pay? Installments for time-to-pay arrangements are taken by direct debt. This is to ensure a smoother process for both customers and HMRC, as it means payments cannot be late. It is likely that HMRC will want the Direct Debit set up on the day of the call. How to qualify for the arrangement HMRC will consider many different criteria when choosing whether to approve a time-to-pay arrangement. These include:Compliance with tax rules and regulations. Actions such as filing taxes late and being fined suggest that your company is unreliable and so unlikely to meet the terms of your agreement. Your line of business/industry Some businesses and industries are higher risk due to competitiveness, past experience and cash flow issues. Past experience of Time to Pay Arrangements, If you have had a Time to Pay arrangement before, you will still be considered, but this may affect your application. VAT taxpayersIn 2024, HMRC changed the eligibility requirements for a VAT Time to Pay arrangement. So now more businesses are eligible to use them.You can set up a VAT payment plan online if you:Owe up to £50,000 Have a debt for an accounting period that started in 2023 or later Seek a maximum period of 12 months to pay off the debt. Do not have any other payment plans or debts with HMRC Are up to date on all your tax returnsYou cannot set up a VAT payment plan online if you use a cash accounting scheme, an annual accounting scheme, or make payments on account.If your company can't pay the corporation tax that is due from the previous year, this can also be included in a time-to-pay arrangement. This situation is more common for those that are contractors/consultants in industries such IT/Banking. If this is you, then call us on 0800 9700539 to talk to an advisor. Research and Development Tax Credits These can be taken into account when agreeing to a TTP, but they have to be finalised and agreed upon. Consequently, they aren't really a relevant negotiating tactic. What could let your company down? Poor compliance with the rules and regulations surrounding your tax affairs, i.e. fines and late filing of paperwork. HMRC will also take into consideration your line of business and their history of meeting TTP arrangements. It only makes sense really that they are going to be less likely to affectively "lend" to business that are deemed high-risk.If your company has had a time-to-pay deal (TTP) in the past, they will still consider you for another TTP. However, HMRC are looking to scale back their level of TTP scheme, as it does not look particularly fair to be raising taxes but not collecting actual tax owed. What if HMRC does not accept a time-to-pay deal you can afford? If you have tried on your own to establish a time-to-pay arrangement and it has been rejected, you should conduct a turnaround advisor immediately. They can conduct an audit of your financial situation, including a statement of affairs and a financial forecast.h3>Time to Pay ArrangementWe can help arrange a time to pay with HMRC. Call us on 0800 9700539 to find out more. Company Voluntary Arrangement Consider a company voluntary arrangement. This will take the pressure off straight away. This allows non tax debts to be partially written off. It also allows your company to cut costs, make redundancies and plan a turnaround. HMRC will accept a CVA if the proposal is fair, and the company is viable. See one of our case studies demonstrating this. The administration or pre pack administration. These very powerful techniques can help protect the business assets and sell them to a new company or third party. This will protect the company from aggressive legal action by HMRC. Other possible optionsA short-term VAT loan (but beware – this can just put off the real decision and many lenders will require a personal guarantee). Refinancing the company through a bank or factoring facility. Injecting personal funds (but only if the business is truly viable going forward).Your advisor will then approach HMRC on your behalf. Their evidence often carries more weight as they will not put forward unrealistic proposals. In addition, advisors such as ourselves talk to HMRC all the time as part of their day job!If this offer of a time-to-pay arrangement is refused but the company is viable, your advisor may suggest proposing a company voluntary arrangement (CVA). This is a formal insolvency tool used to restructure businesses and debts and recover from cash flow issues.Sometimes the threat of insolvency, in the form of a CVA, can push HMRC to accept a time-to-pay agreement. This is because with a CVA the return will be over a 3–5 year period. Also, if the business did eventually become insolvent, HMRC may be left with nothing at all. Therefore, it is possible to persuade HMRC that a time-to-pay agreement is the best way to ensure it recovers all of the company's outstanding taxes within a reasonable time frame.

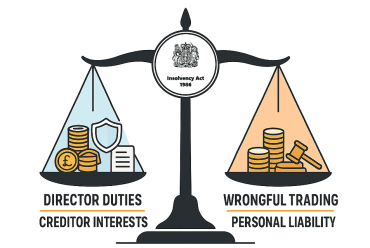

ReadAm I Trading Whilst Insolvent? – Directors Guide To The Risks

Trading whilst insolvent is a legal term used to describe a business which continues trading when it cannot pay its debts and its liabilities are greater than its assets. It can lead to a breach of several provisions of the Insolvency Act 1986 which can result in the directors being held personally liable

Read

Wrongful Trading – Director Liability & How to Avoid It

Wrongful trading is where an insolvent company has continued to trade in a way which worsens the position of the creditors that any reasonable director would not have allowed.

Read