Can’t Pay Fleximize Loan

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Director of RMT Recovery & Insolvency

ReadCan’t Pay Fleximize Loan

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Director of RMT Recovery & Insolvency

Read

Company In Financial Trouble? Expert Advice For Worried Directors

If you’re struggling to meet debt payments and cashflow is suffering, don’t panic! There are a number of options available to help turnaround the business or company if it is in financial trouble.

ReadCan’t Pay Funding Circle, Bizcap or Iwoca Loan

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Director of RMT Recovery & Insolvency

ReadDirectors Disqualification A Guide For Worried Directors

The content on this page has been written by Keith Steven and approved by Chris Ferguson Licensed Insolvency Practitioner and Director of RMT Insolvency and Recovery.

ReadCheapest Way To Liquidate a Company

The cheapest we can liquidate a company for is about £4.5k + VAT. This would be for a company with only a couple of creditors such as HMRC and a Bounce Back Loan.

Read

HMRC VAT Security Deposits for Struggling Companies

We have received a letter from HMRC and they have demanded a security deposit. What does that mean?

Read

Company Bankruptcy Advice

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Managing Director of RMT KSA

Read

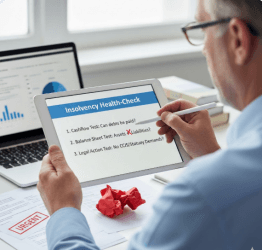

Is My Company Insolvent? The 3 Legal Tests & Director Duties

There are 3 tests to check to see if a company or business is insolvent. The cashflow test, balance sheet test and the legal action test.

Read

What is Balance Sheet Insolvency?

Balance sheet insolvency is when a company’s total liabilities outweigh its total assets. However, it may still be able to pay its liabilities when they are due.

Read

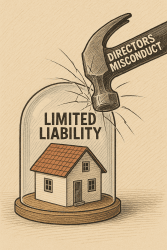

If My Company Goes Bust Will I Lose My House?

You will not lose your house if your company goes bust but if you have been guilty of defrauding creditors or have personally guaranteed company loans then it is possible.

ReadTrading Whilst Insolvent? – Directors Guide To The Risks

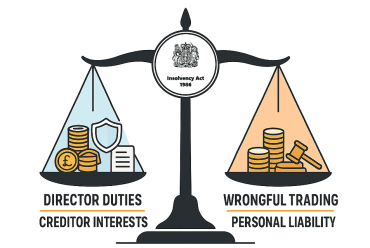

Trading whilst insolvent is a legal term used to describe a business which continues trading when it cannot pay its debts and its liabilities are greater than its assets. It can lead to a breach of several provisions of the Insolvency Act 1986 which can result in the directors being held personally liable

Read

Wrongful Trading – Director Liability & How to Avoid It

Wrongful trading is where an insolvent company has continued to trade in a way which worsens the position of the creditors that any reasonable director would not have allowed.

Read