Can’t Pay Corporation Tax – What Are Your Options

If you can't pay your corporation tax, then it may be that the company is insolvent. Get in touch with HMRC to explain the situation.

ReadCan’t Pay Corporation Tax – What Are Your Options

If you can't pay your corporation tax, then it may be that the company is insolvent. Get in touch with HMRC to explain the situation.

ReadReceived An HMRC Notice Of Enforcement?

Any creditor who is owed money has the power to serve a Notice of Enforcement if they obtain a court order. HMRC or landlords do not need a court order, however they must still obey strict regulations to retrieve debt.

ReadWhat is an HMRC Notice Of Enforcement?

Any creditor who is owed money has the power to serve a Notice of Enforcement if they obtain a court order. HMRC or landlords do not need a court order, however they must still obey strict regulations to retrieve debt.

ReadHMRC Bailiffs and Enforcement Officers – Can They Enter My House?

A Bailiff, HMRC officer or an Enforcement Officer has the power to take control of your goods and possessions in order to satisfy a debt.

ReadHow To Get Help With VAT Arrears

Is your business suffering from VAT arrears? Failure to pay VAT on time can lead to problems with HMRC who will try and recover the debts. We can advise on your options

Read

Penalties for Late Payment of PAYE

HMRC implement penalties for late payment of periodic PAYE /NIC from businesses.

Read

What are PAYE Security Deposits?

Since 6 April 2012 HMRC have been able to demand PAYE security deposits under paragraph 4(2)(a) of Schedule 11 to the VAT Act 1994.

ReadWhat Is The HMRC Debt Management Department

The content on this page has been written by Robert Moore and approved by Chris Ferguson Licensed Insolvency Practitioner and Managing Director of RMT KSA

ReadHow HMRC Collects Its Debts: A Guide for Businesses

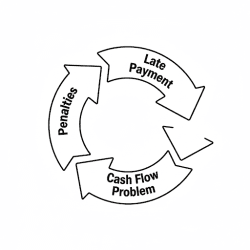

HMRC is what is called a “sophisticated creditor” in that they have economies of scale that ensure that it is worth their while to chase even the smallest of debts. There is no particular difference in the methods used for collecting different types of taxes, but VAT and PAYE are often pursued more readily as they make up the largest types of tax that a company pays.So, what steps are taken by HMRC to ensure payment is made?Step 1: Reminders and Collections In the first instance, HMRC will start collecting debts by issuing payment reminders and these can be in the form of letters and even SMS texts. If you fail to pay the amount owed, the debt may be outsourced to a third-party debt collection agency.HMRC has started to use these private-sector debt collection agencies more and more in recent years to pursue debts. These agencies are likely to send more aggressive reminders, threatening legal action or the seizure of goods.HMRC Debt Collection Agencies include:1st Locate (trading as LCS) Advantis Credit Ltd Bluestone Credit Management Ltd BPO Collections Ltd CCS Collect (also known as Commercial Collection Services Ltd) Moorcroft Oriel Collections Limited Past Due Credit Solutions (PDCS)Step 2: Control of Goods (Distraint) If initial reminders do not work, HMRC or a certified bailiff contracted by them may take action to take control of goods or property at the company's registered address. This is a formal process known as distraint. The goal is to sell the goods at auction to settle the debt.The officer will send a Writ of Control and a Notice of Enforcement to the debtor, giving them 7 clear days to either pay in full or negotiate a payment plan. If the debtor doesn't sign a Controlled Goods Agreement, the officer can make arrangements to remove the goods for sale.While the value of goods may not be enough to cover the debt, the threat of seizure is often enough to focus minds and find funds from elsewhere.Step 3: A Winding-Up Petition If all other methods fail, HMRC may issue a winding-up petition as a last resort. This means HMRC will instruct its solicitors to petition the court to rule that the business is insolvent and should be closed.A winding-up petition prevents the debt from getting any worse, as the company will be forced to stop trading. In most cases, it is unlikely that HMRC will get its money back, but the threat of this action can be very effective.

Read

Plan A for Companies or Partnerships; Avoid Insolvency

Is there a way that I can avoid formal insolvency? Yes, Plan A for companies or partnerships; An informal deal with creditors, coupled with possible refinancing Using the threat of the insolvency options can be like the proverbial Sword of Damocles , you can wind the company up, possibly go personally bankrupt or enter an IVA but the creditors would undoubtedly see a compromise or even complete discount of their debts if that occurred.Being prepared to argue with creditors that the informal route means at least some if not all of their debt is recovered and that this approach will allow you to practice in future, is the common sense solution.RMT will always however make sure that the options of company voluntary arrangement and liquidation have been assessed, a statement of affairs prepared and valuations of any properties obtained to counter the why wait for money what if we simply wind the company up? question. The main thing to remember is we are prepared for their aggressive questioning.So pointing this out bluntly, allows us to prepare a plan for the recovery of the creditors monies over a considerable period of time say 12-24 months. Yes even if HMRC has rejected YOUR suggested time to pay proposals.We would generally insist on the following work being part of our restructuring brief;Detailed DAILY CASHFLOW we can provide the tools and assess this for the company. But this MUST be introduced and to help survival you or your admin people must update every day. Statement of affairs for the company. Probably requires a desk top valuation of any corporate property. RMT will do this confidentially as part of the brief. Detailed financial forecasts for the business. What if scenario planning ie what if turnover falls, WIP is not all collected for example? Negotiations with the creditors (usually HMRC and the bank) in person and where required in writing led by KSAs experienced debt negotiators. Possible assessment of your personal property and assess possibility of new debt from property(ies)This process can be delivered in 1-3 weeks from engagement and is led by very pragmatic experts in this field. Before commencing we will set out the strategy plan in writing. This work is always costed in writing in our unique solutions report which is provided FREE after your first meeting with a RMT Director or Regional Manager.Call RMT on 08009700539 for detailsA word of warning. If your company or limited liability partnership has relied upon multiple time to pay deals over recent years with HMRC and these deals have regularly not been adhered to, then this first option may not succeed, but we believe it is still worth trying.

Read