Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up Petition

Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up PetitionAn accountancy, tax and business services company had built up a long-established client base over many years. The founding director was an experienced chartered accountant who had previously worked at a major accountancy firm before setting up his own practice.

The business grew steadily, but the director later suffered serious health problems, and periods of hospitalisation. During these absences, HMRC compliance deteriorated. VAT and PAYE matters were not dealt with properly, returns were missed, and historic tax arrears began to build up.

The director later decided to sell the majority of the business, partly because of age and health concerns and partly because the practice needed new energy and day-to-day management. The core business and most of the company’s assets were sold to a team led by senior staff. However, the sale was structured with deferred consideration rather than a full upfront payment.

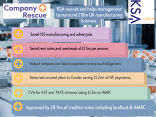

This meant that significant value remained due to the company, but it would be received over time. At the date of the CVA proposal, the deferred consideration still due was approximately £343,000. The company continued to trade in a much reduced form, retaining a small number of clients and some specialist consultancy work, but it did not have enough immediate cash to settle historic HMRC arrears and other creditors.

HMRC issued a winding-up petition, creating a serious risk that the company could be pushed into compulsory liquidation before the deferred consideration was fully collected. This would have risked destroying or reducing value that could otherwise be used to repay creditors.

RMT was instructed to advise on the company’s options. A Company Voluntary Arrangement was proposed as a holding CVA. The aim was not simply to rescue a trading business in the usual way, but to create a controlled structure that allowed time for the deferred consideration to be collected and paid to creditors.

The CVA was funded by monthly contributions from the deferred consideration and reduced ongoing trading, together with a one-off contribution of £130,000 from the director, raised through the remortgaging of a personally owned commercial property. The director also agreed to take only a modest salary to keep overheads to a minimum.

The CVA was designed to pay creditors in full over three years. HMRC, as a secondary preferential creditor, was forecast to receive 100p in the £, and unsecured creditors were also forecast to receive 100p in the £.

This case demonstrates how a CVA can be used creatively where value is tied up in deferred consideration. Rather than allowing a winding-up petition to force a premature liquidation, the CVA created a structured route to preserve value, collect future payments and repay creditors in full.

Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up Petition

Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up Petition

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company