Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

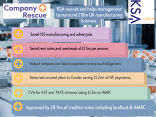

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryAn online retail company with a turnover of approximately £2.6 million faced a significant financial crisis due to a combination of factors. The company was undercapitalised, had excessive and unproductive advertising costs, and was burdened with high staff costs in a competitive market. The board had identified these issues and had already taken steps to cut staff and reduce costs, but the cash flow pressures persisted. The company had a total unsecured debt of £830,000, with HMRC holding a 33% share of this. The directors were also at personal risk due to personal guarantees on various creditors’ facilities. A major complication was a substantial overdrawn directors’ loan account (ODDLA) that the directors were not in a position to repay from personal funds while also managing other personal liabilities. The situation was made even more urgent when a creditor served a statutory demand with the threat of a winding-up petition, pushing the company to the brink of liquidation.

In January 2015, the directors contacted RMT KSA, who was appointed to assist with a Company Voluntary Arrangement (CVA). RMT KSA immediately negotiated with the creditor who had issued the statutory demand, successfully preventing the winding-up petition from being presented. The CVA proposal was a multi-faceted solution that aimed to address the company’s liabilities and operational issues. The company changed its stocking policy to reduce stock days, implemented a rigid stock control protocol, and reduced marketing spend. Critically, KSA also assisted the directors in proposing Individual Voluntary Arrangements (IVAs) to address the ODDLA and the shortfall on balances from personal guarantees. These IVAs would provide additional contributions to the CVA. The CVA also included using the legal mechanism to cancel two asset-based lending agreements, a key measure to reduce costs. The CVA proposal offered a repayment of 50p in the £1 to creditors over six years, with contributions from the directors’ IVAs.

The CVA process was approved and filed, but not without a fight. Initially, HMRC rejected the proposal. RMT KSA appealed this decision, and at the creditors’ meeting, it was agreed to adjourn for two weeks to allow for further negotiations with HMRC. The effort paid off, as HMRC responded with a revised proposal that included a minimum 55p in the £1 dividend, which was accepted by the directors. Additional modifications from other creditors were also agreed upon, and the CVA and IVAs were unanimously approved at the adjourned creditors’ meeting. This outcome provided a legally binding framework for the company’s recovery, allowing it to continue trading and saving 13 jobs. The CVA was instrumental in helping the company navigate its complex financial situation, manage its debt, and restructure its operations for long-term survival. The case demonstrates that even with significant opposition and personal financial risk, a well-structured CVA and IVA can provide a viable path to recovery.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!