Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

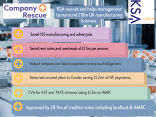

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryAn IT company, with turnover falling by £700,000 to approximately £1.3 million in 2009, faced a severe financial crisis. Despite having a high number of enquiries and quotations, a gap between sales and cash flow led to insolvency. The company was burdened with a total unsecured debt of £230,000. Of this debt, HMRC was owed 18.3%, a significant amount but not a majority. A key issue was an outstanding finance agreement for a company asset. The sole director had also provided a personal guarantee to a secured creditor, which placed him at significant personal risk. To make matters worse, the company was also in debt to various connected creditors, including the directors themselves, for approximately £75,000 in loans.

In October 2009, the director contacted KSA, who was appointed to assist with a Company Voluntary Arrangement (CVA). The CVA was designed as a comprehensive solution to the company’s financial problems. Prior to KSA’s appointment, the company had already made two redundancies to cut costs, and KSA assisted with another one. A new purchase protocol was instigated to ensure value, and credit control was tightened to ensure all debts were collected within 30 days. As part of the CVA, the connected creditors agreed to waive their claims to the £75,000 they were owed. KSA also assisted the directors in cancelling the outstanding finance agreement. The CVA proposal offered a repayment of 35p in the £1 to unsecured creditors over five years, a plan that aimed to be fair to creditors while allowing the company to survive.

The CVA was accepted by the body of creditors in late March 2010. The approval provided the company with the legal framework it needed to continue trading and address its debts. By implementing the CVA, the company was able to make the necessary cost cuts and tighten its financial controls. This led to a positive turnaround in the business’s fortunes. The company’s recovery was so successful that in April 2014, a revision to the CVA was proposed to and approved by creditors. The company offered to make a one-off payment in full and final settlement, which allowed it to complete the CVA one year early. This case demonstrates that a CVA can be a highly effective tool for a company with cash flow problems, providing a clear path to not only recovery but also early success and freedom from its financial obligations.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!