Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryA successful retail company, specializing in alternative fashion and body piercing services, faced a significant downturn due to the 2009 recession. The company had expanded by leasing several new shop premises during a more prosperous period. However, as the economy soured, many of these stores began underperforming. The high rents on these properties became a major financial drag, pulling down the company’s overall profitability. The business was burdened with leases that were too expensive and inflexible, creating a crisis that threatened the viability of the entire company. The challenge was to restructure the business to shed these unprofitable locations and their associated high costs without forcing the company into a full liquidation.

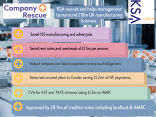

In consultation with KSA, the company decided to use a Company Voluntary Arrangement (CVA) as the ideal vehicle for a radical restructuring. The CVA provided the legal flexibility needed to close individually unprofitable stores. As part of the plan, three stores were closed, resulting in an annual saving in rent and rates of over **£200,000**. This difficult decision also led to redundancies, but it reduced the annual wages bill by over **£121,000**. For several other stores, the company opted to negotiate with the landlords for rent reductions instead of closing them. These negotiations were successful, with landlords agreeing to new, more favorable leases, including a significant rent reduction and a flexible two-month notice period. The CVA also incorporated the agreed-upon dilapidations claims from the original leases, with a cap on future claims, which provided further financial certainty.

The meticulously prepared CVA proposal was put before creditors and was successfully accepted at the creditors’ meeting. This acceptance allowed the company to execute its restructuring plan, which not only shed the unprofitable stores and their costly leases but also secured more viable terms for key locations. The strategic use of the CVA enabled the business to address its most pressing financial burdens—unsustainable rent and rates—without undergoing liquidation. The company was able to downsize to a profitable core of stores, securing its future and preserving the jobs of the remaining employees. This case demonstrates the power of a CVA as a tool for strategic rationalization, enabling a company to terminate onerous contracts and reposition itself for long-term profitability.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!