Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryA successful leisure travel company, with sales of £13 million prior to 2020, was hit hard by the COVID-19 pandemic. The board initially forecast a sales drop to around £4 million, but new bookings evaporated with the onset of lockdowns. The company was suddenly faced with a demand for thousands of refunds and credit notes, a major cash drain, especially after a significant investment in new IT systems had already depleted its cash reserves. The situation was further exacerbated by subsequent lockdowns in late 2020 and early 2021. The key stakeholders—including a trade insurance company refusing to pay out, landlords of an oversized property, and tens of thousands of customers demanding refunds—created a highly complex and challenging environment for the company. They were in an unprecedented crisis with limited financial maneuverability and significant pressure from all sides.

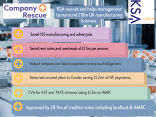

KSA was approached in March 2020 to develop a creative solution. The company, armed with excellent management information and a strong external FD, embarked on a deep-reaching restructuring plan centered on a Company Voluntary Arrangement (CVA). This was groundbreaking, as ABTA had never before allowed a company in a CVA to maintain its cover. The strong expected future growth and the management team’s impeccable compliance record, however, convinced ABTA to listen. The CVA proposal offered a 100p in the £1 dividend to repay almost £7.5 million of creditors over four years. This ambitious plan was crucial to securing the support of all stakeholders. The restructuring also involved making 40 out of 85 employees redundant, reducing staff costs to fit the new business reality. A significant number of online meetings—over 50 in six months—were held to navigate the complexities of the plan while everyone was working from home.

The CVA was approved by creditors in September 2020. The company managed to satisfy its creditors and stakeholders: a modest number of customers received refunds, over 4,000 received insurance payouts, and thousands were provided with a delayed product. Crucially, no customers lost out, which was a core objective. Despite not meeting initial sales forecasts in the year post-CVA (sales were £6.8m), the business survived. By early 2022, facing a new challenge of rising customer demand, the company needed to increase its ABTA bond from £1.5m to £2.5m. With the debt market for a company in a CVA being negligible and turnaround equity requiring a significant share dilution, the directors made a bold decision. They unilaterally re-mortgaged their own homes to raise new capital, which was then secured to the company, and registered in their names. This capital injection allowed the company to meet its bond requirements. The business is now trading well, with record sales of £18m and a pre-tax profit of £1.2m in FY 2022. The company is on track to pay all its creditors in full, a testament to the resilient management team, the quality of financial information, and a solid plan.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!