Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

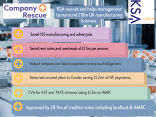

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryA fast-growing, multi-depot company with sales of around £30 million faced a critical cash flow crisis in late 2009. The core problem was a lack of reliable financial data, stemming from outdated DOS-based systems and poor management information (MI). The directors, despite their experience, were unable to accurately forecast the impact of a series of unfortunate events on the company’s solvency. These included a major bank, RBS, restricting drawdowns on its invoice finance facility, a four-month tax arrears deal with HMRC, and a number of unexpected external factors. In 2011, severe snow brought operations to a standstill, followed by rising fuel prices that the company’s slow systems couldn’t recover quickly enough. A major customer moved its accounts payable to India, causing delayed and incorrect payments. These factors, combined with several bad debts, created a relentless cash flow squeeze that led to a new, unmanageable tax debt. With HMRC unwilling to agree to another time-to-pay deal, the company was in a dire situation.

Recognizing the fundamental problem was poor financial data, the company’s board, advised by KSA Group, made a significant investment in a financial overhaul. They hired a new, experienced finance director to replace the old systems with modern, Windows-based ones. This allowed them to analyze vast amounts of transactional data, providing a clear picture of the business’s profitability on a per-depot basis. Two depots were closed as a result of this analysis, and a project was launched to analyze every aspect of customer and operational efficiency. The company also successfully replaced its RBS facilities with Close Invoice Finance, renegotiating better terms. When a new tax debt accumulated and HMRC refused a time-to-pay deal, the company chose to pursue a Company Voluntary Arrangement (CVA) as the only viable option to save the business and repay its creditors.

Despite an independent business review (IBR) firm advising the bank that a CVA would not be achieved, the company proved them wrong. The CVA was approved with over a 99% vote in favor, including HMRC, which held over £1.5 million in tax liabilities. The CVA provided for initial monthly payments of £9,000 and a proposed dividend of 38p in the £1 over five years. This outcome demonstrated that even a business with poor financial data can be rescued. The company’s investment in its internal systems was a key factor in the turnaround, as it allowed the directors to make informed decisions that led to cost-cutting and improved profitability. The case study is a powerful reminder that while external factors can create a crisis, a company’s ability to understand and control its internal data is paramount to its survival. The CVA provided a critical safety net that allowed the company to implement its turnaround plan and return to a position of financial health.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!