Construction Company Avoids Insolvency After HMRC Agrees £249k Time to Pay Arrangement

Construction Company Avoids Insolvency After HMRC Agrees £249k Time to Pay ArrangementAn engineering company with a turnover of approximately £2.1 million in 2011 faced a severe financial crisis. The company was undercapitalised and its problems were compounded by the 2008 credit crunch, which caused a series of falling and delayed orders. A major blow came in late 2010 with a bad debt of £320,000, followed by a poorly managed contract that resulted in a £100,000 loss. These issues led to a total unsecured debt of £680,000, with HMRC accounting for a significant 44% of that total. The director’s personal financial health was also at risk due to personal guarantees on loans from the bank and an invoice finance company. The situation escalated to a crisis point when a creditor served a winding-up petition, which threatened to shut down the business and leave unsecured creditors with nothing. The company needed a comprehensive solution to manage its debts and restore stability.

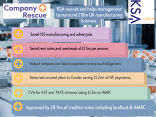

In August 2011, the company engaged RMT KSA to assist with a Company Voluntary Arrangement (CVA). This was the central component of a multi-faceted rescue plan. RMT KSA immediately negotiated with the creditor who issued the winding-up petition, successfully getting it withdrawn before it could be advertised. The company implemented a number of rigorous cost-cutting measures, including a new regime to reduce energy waste, and a strategy to reduce equipment hire costs by eliminating non-essential items. Some senior managers accepted a temporary salary reduction, and the company froze shop floor wages to control costs. A key action was using the CVA to vacate one of its leased units, which generated significant savings on rent and rates. The company also ceased unprofitable direct export orders to focus on UK-based contracts. The CVA proposal offered a repayment of 42 pence in the £1 to unsecured creditors over five years, which would be a far better return than a liquidation would have provided. The director, as a connected creditor, also agreed to waive their claim to £150,000 in loans they had made to the company.

The CVA was successfully approved at an adjourned creditors’ meeting in late January 2012. Although HMRC initially rejected the proposal, KSA’s negotiations and presentation of the company’s strong order book (worth approximately £1.8 million at the time) were successful, leading to HMRC’s approval with some standard modifications. The CVA provided a legal and structured framework for the company’s recovery, allowing it to continue trading and saving 29 jobs. The company successfully managed its debt, reduced its overheads, and returned to profitability. This case demonstrates that a CVA can be a powerful and effective tool for a company with a fundamentally sound business model to overcome significant financial setbacks, gain breathing room from creditors, and secure its future.

Construction Company Avoids Insolvency After HMRC Agrees £249k Time to Pay Arrangement

Construction Company Avoids Insolvency After HMRC Agrees £249k Time to Pay Arrangement

Holding CVA Used To Preserve Deferred Consideration And Repay Creditors In Full

Holding CVA Used To Preserve Deferred Consideration And Repay Creditors In Full

Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up Petition

Midlands Solicitors’ Firm Saved By CVA After HMRC Winding-Up PetitionTransport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!