Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

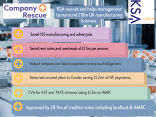

A motor trade company specializing in used car sales and servicing faced a significant financial crisis despite a previous year’s turnover of around £5.4 million. The core issues stemmed from a critical downturn in sales and falling turnover, exacerbated by a highly competitive market and the business being undercapitalized. With an unsecured debt of £612,000, 73% of which was owed to HMRC, the company was in a precarious position. The director had also provided personal guarantees to various creditors, placing their personal assets at risk. Without intervention, the business was likely to fail, leading to job losses and a complete collapse of operations.

In May 2014, the company engaged KSA to explore a Company Voluntary Arrangement (CVA) as a viable solution. The CVA process involved a series of strategic actions to restructure the business and reduce its debt burden. A crucial step was a significant cost and overhead reduction. This included making several staff redundancies, which had a ripple effect in lowering associated costs. The director also proactively cut ineffective marketing and promotional expenses. The CVA proposal, lodged in court in December 2014, offered to repay 41 pence for every £1 of unsecured debt over a five-year period. While the largest creditor, HMRC, initially rejected the CVA, the creditors’ meeting was adjourned to allow the company to address HMRC’s concerns, ultimately securing their approval.

The CVA was successfully approved at the adjourned creditors’ meeting in January 2015. This outcome enabled the company to continue trading and avoid liquidation, despite its immense debt. The successful negotiation with HMRC, which held a majority of the unsecured debt, was a critical factor in the CVA’s approval. By implementing the cost-cutting measures and restructuring its finances, the company was able to stabilize its operations and provide a clear, manageable repayment plan to its creditors. The CVA’s success not only saved the business but also protected the jobs of 14 employees and provided a formal, legal framework for the company’s financial recovery.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV ManufacturerMedium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Medium Sized Law Firm Ran Into Trouble By Expanding Too Fast

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!