Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

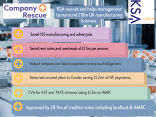

Transport Company Facing Difficulty Following Foray Into Direct Home DeliveryReds Technologies, a company trading as The Energy Conservation Group, with a predicted turnover of £3.3m for the coming year, was facing a number of critical issues. The business was **undercapitalised**, which made it difficult to invest in sales and marketing. A major problem was a sharp reduction in credit facilities across its supply chain, with one main creditor reducing its limit from £350,000 to £60,000. This was compounded by a continued government reduction in Feed-in Tariffs, increased competition, and a tough trading period during the summer of 2012. The company’s turnover had already fallen from £9.6m in 2011 to £9m, and a further sharp drop was anticipated. The directors were owed £1.2m and held registered security for these loans, which, in the event of insolvency, would give them significant voting power.

The CEO, Simon Booth, contacted KSA Group, and a meeting was held in August 2012. KSA was appointed to assist the company with a Company Voluntary Arrangement (CVA). Prior to KSA’s appointment, the CEO had already implemented a number of restructuring policies, including making nine redundancies to cut overheads. The CVA was proposed as a way to formalize this restructuring and address the company’s debts. The CVA would have allowed the company to contain creditor pressure and provide a structured plan for repayment. The plan also aimed to leverage the directors’ significant financial stake in the company to help influence the CVA vote. The company also had a small amount of unsecured trade debt, around £550,000, which would be managed under the CVA.

The CVA process was ultimately not pursued. Based on recent trading performance and a lack of confidence in future viability, the directors concluded that a CVA was no longer a viable option. They then sought further advice from KSA regarding alternative insolvency routes. KSA was appointed to liquidate the company via a Creditors Voluntary Liquidation (CVL) in November 2012. While the company could not be saved, the CVL provided a clean and professional conclusion. It minimized the personal risks to the directors and ensured that all creditors were treated equally. This case demonstrates that even when a CVA is not the final solution, professional advice is crucial for navigating a company’s financial crisis. A CVL, in this instance, was the most sensible course of action, allowing the directors to wind up the business responsibly when the prevailing business climate proved too difficult for continued operations.

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Transport Company Facing Difficulty Following Foray Into Direct Home Delivery

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Engineering and Design Group of Companies Suffered From Bad Debt From EV Manufacturer

Haulage and Logistics Company Needing To Make A Profit

Haulage and Logistics Company Needing To Make A Profit

£18m T/o Pharmaceutical Manufacturing Company

£18m T/o Pharmaceutical Manufacturing Company

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!

RMT Rescues 3 Large Companies in 3 Months. We Can Help Your Clients!Sports Clothing Distributor Sales £7m Struggling Due To Brexit

Sports Clothing Distributor Sales £7m Struggling Due To Brexit