When might a CVA be appropriate for a company?

A Company Voluntary Agreement can be a viable option for businesses facing financial difficulties, but it’s not suitable for every situation. To qualify for a CVA, a company must generally meet the following criteria:

- The company must be insolvent or contingently insolvent (unable to pay its debts as they fall due).

- The core business must be fundamentally sound with potential for future profitability.

- The company should have a reliable and predictable income stream.

- The company must be compliant with tax and regulatory obligations.

- A dedicated and experienced management team is essential to implement the CVA successfully.

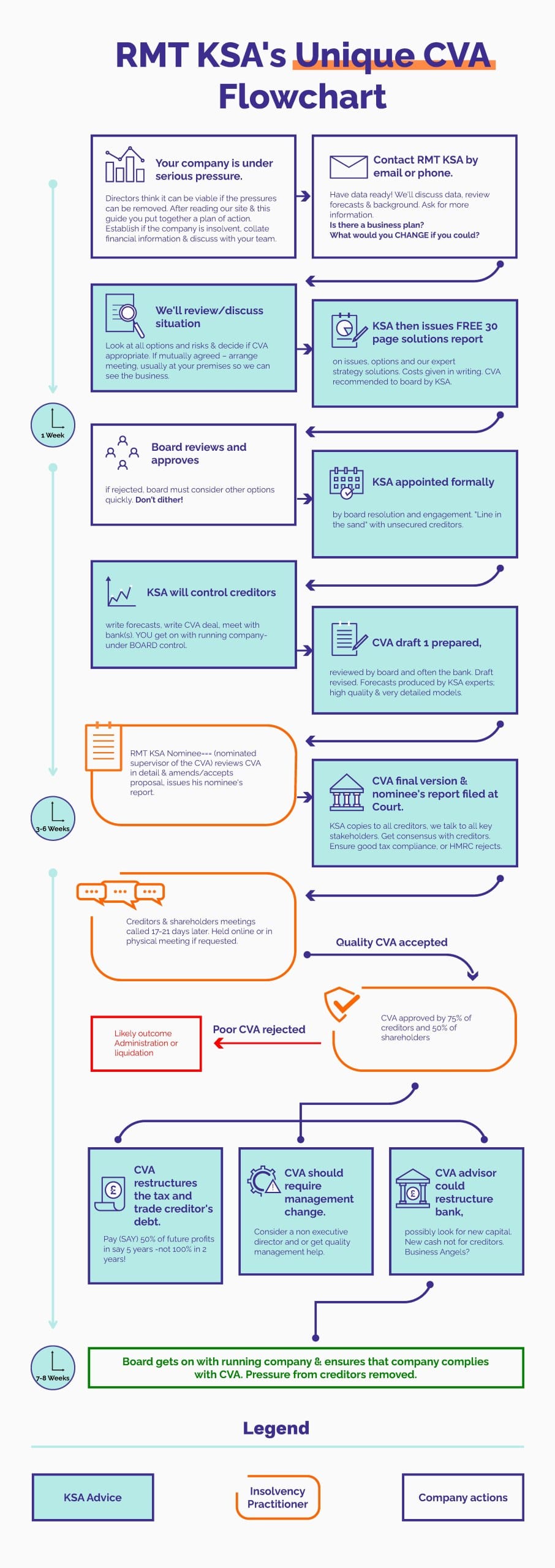

A step by step process of putting a company into a CVA

Read our breakdown of the CVA process below

Step 1: Appoint Experienced CVA Advisors

First, you should select experienced turnaround practitioners or insolvency practitioners to guide your CVA process. They should be regulated by the Insolvency Practitioners Association, The Institute of Chartered Accountants England and Wales, or The Insolvency Service and have a strong track record of successfully carrying out CVAs for their clients.

Step 2: Company Review

Your advisors then conduct a thorough review of the business, preparing detailed proposals, a statement of affairs and financial forecasts. If your financial and accounting information is poor or non-existent, your company may not suitable for this process.

Step 3: Proposal Drafting Period

While the proposal is being put together, companies should carry out the following guidelines to increase their chances of a successful outcome:

- Continue normal business operations, paying suppliers for new goods and services.

- Collect outstanding debts and manage cash flow to ensure sufficient liquidity.

- Implement cost-cutting measures, including reducing staffing levels or renegotiating

contracts, to improve the company’s financial position.

In addition, your company typically will not need to pay PAYE, NIC or VAT in this hiatus period.

However, it is wise to start paying these taxes if the CVA preparation is taking a considerable time to demonstrate viability to HMRC.

Step 4: Talk To Secured Creditors

Though they are not bound by the CVA, it is a good idea as the CVA is being proposed to keep secured lenders informed. Showing them that you are on the way to putting the company on better footing will prevent creditors worrying about their exposure. Our expert advisors will liaise with the lenders to ensure they are fully appraised of the proposed financial and cost changes and the structure of the CVA plan.

Step 5: Proposal Finalisation

Once ready, the nominee (licensed insolvency practitioner) reviews and approves the CVA proposal to ensure that it’s appropriate, achievable, and maximises creditors’ interests. This report is then filed in the Insolvency and Companies Court and is given a Court Originating Application number.

Step 6: Creditor Consideration

All creditors receive the proposal for consideration over a 17-28 day review period.

Step 7: Creditors Meeting and Voting

At the creditors meeting, the creditors vote on the proposal; the CVA is approved if 75% of creditors vote in favour (whether in person or by proxy). Do remember it is not 75% of all creditors, it is 75% by value of those votes cast at that meeting. If creditors have approved the proposal, it is carried whether shareholders approve or not.

Step 8: Approval and payment to creditors

Once approved, the voluntary arrangement becomes legally binding on all creditors. Directors maintain control while making agreed monthly payments administered by the supervisor.

Provided the company conforms to the proposal and makes its monthly CVA contributions, then the CVA continues for the agreed period. Failure to keep up with contributions can lead to the arrangement being aborted, usually resulting in liquidation or administration.

How Long Does It Take To Implement A CVA?

It should take 3-4 months to implement a Company Voluntary Arrangement, from start to finish. To speed up the process, it’s essential that company directors are organised and efficient in responding to the requests of their advisors. The quicker information gets to them to build a statement of affairs, the quicker the proposal can be filed in court.

How long does my company have to be in a CVA?

A CVA typically lasts for between 3-5 years so it is not an undertaking to be taken lightly. During this period, HMRC debts (VAT and PAYE) must be repaid first, usually within years 1-4. Other unsecured creditors then receive between 5p-100p per pound, depending on the company’s

repayment capacity.

In some cases you can hive the business. What this means is that the business can be transferred to a new company while the old entity receives management fees to repay creditors through the CVA. This innovative restructuring needs to be carefully planned, which is why USING SPECIALIST EXPERT CVA ADVISORS, SUCH AS RMT, who own this site IS ESSENTIAL

What happens at the end of the CVA period?

Once the agreed period is completed and the supervisor has issued a completion certificate, then the company leaves the CVA state. Any remaining unsecured debts (where partial repayment was approved) are written off and the directors continue to run the business for the shareholders.