Definition and Differentiation

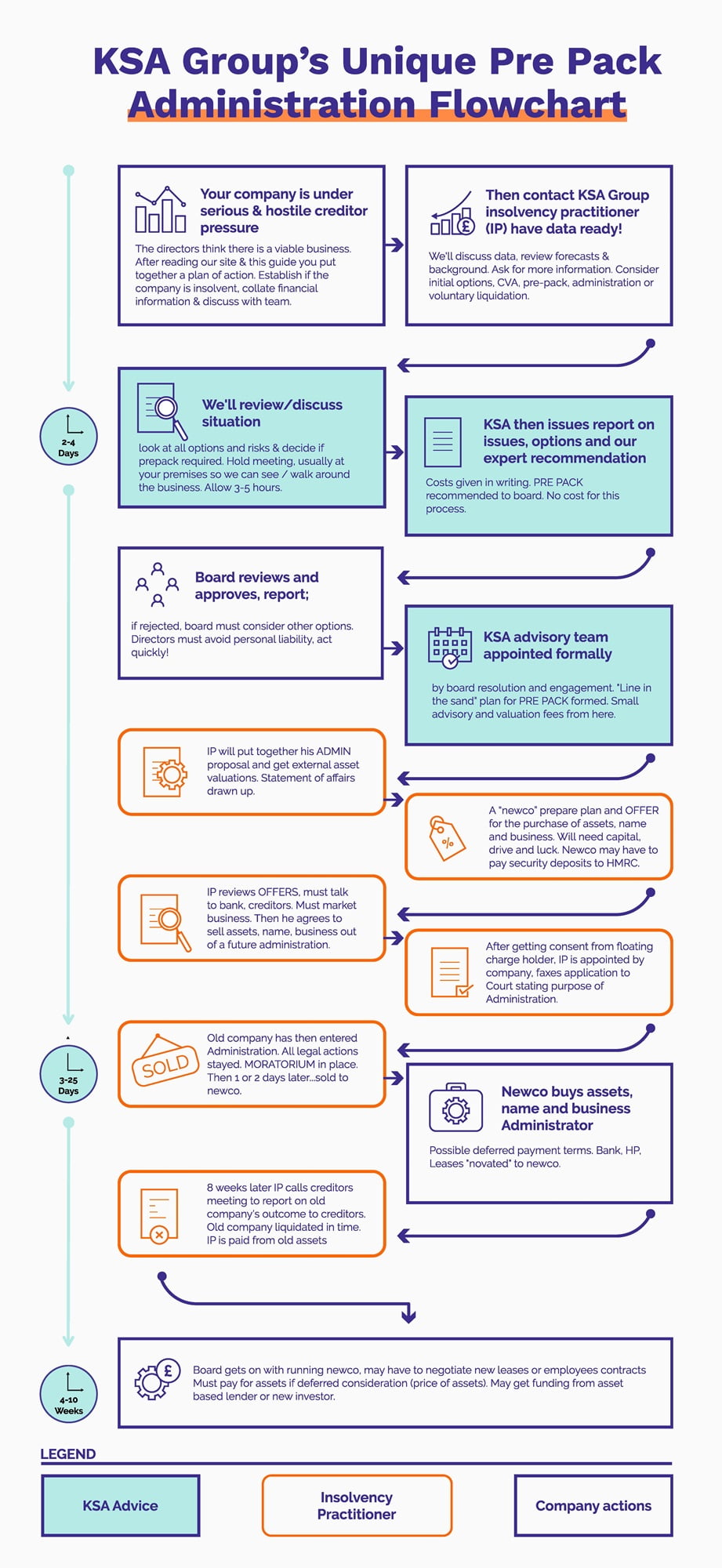

Pre-pack administration is an insolvency procedure which permits an insolvent company to sell its assets to a buyer either immediately upon or within a few days of the administrator’s appointment.

The essential difference from standard administration lies in the timing of the sale of the business and assets. The transaction is negotiated and agreed upon prior to the administrator being formally appointed. This constitutes a powerful, legal mechanism for selling the business to a trade buyer, a third party, or the existing directors operating under a new company (‘newco’).

The ‘newco’ must demonstrate viability and secure funding to acquire the assets of the old company (‘oldco’) at fair value. This procedure offers a swift solution to the threat of a winding up petition; however, it is not permitted after a petition has been issued.

When You Should Seek Advice

The following are key signs that your company may be insolvent:

- Threats emanating from landlords.

- HMRC demanding payment for outstanding PAYE and VAT liabilities.

- Warnings issued by the bank or trade creditors.

- Directors expressing concern about wrongful trading and personal risk.

- The business having onerous contracts, excessive property holdings, a surplus of employees, or having sustained loss of market share or customers.

Suitability of Pre-Pack Administration

Pre-pack administration is most suitable for larger companies due to the complexity and associated costs. It is primarily applicable where there is a severe, immediate threat to the company’s ability to continue trading, such as a critical supplier withdrawing support or the threat of a winding up petition. A viable underlying business capable of attracting necessary funding is a prerequisite.

Process and Procedures of A Pre-Pack Administration

Step 1. Consultation and Resolution

Consultation with licensed insolvency practitioners is the initial step. The resulting advice should be comprehensive and presented in writing for the board. SIP 16 rules mandate that all options—including CVA, trade sale, refinancing, administration, creditors voluntary liquidation, and pre-pack administration must be fully considered. If the board decides to proceed, a formal resolution must be passed instructing the directors to consider the option in greater detail and to appoint necessary advisors.

Step 2. Development of the New Company Business Plan

Should the plan involve selling the business to a ‘newco’, a detailed business plan must be drafted. This document must includ profit and loss, cashflow, and balance sheet forecasts to indicate working capital requirements. The proposed administrator will require this evidence to establish the new company’s viability.

Step 3. Compliance and Regulatory Requirements

Insolvency practitioner guidelines require the IP to market the business to fulfill their fiduciary duty to creditors. This essential step may expose the business to competitive bidding and the risk of sale to a competitor. Formal valuations of assets, intellectual property, and goodwill by RICS qualified surveyors are mandatory.

Sales to connected parties (such as existing directors) are governed by The Administration (Restrictions on Disposal etc. to Connected Persons) Regulations 2021. This requires an independent evaluation and the filing of a SIP 13 report. Critically, this independent evaluator is typically selected by the company’s directors from a pool of experts and must complete their examination within 48 hours for a fixed fee, ensuring compliance is swift and cost-controlled. Directors must seek separate legal advice on how to oversee personal conflict-of-interest risks.

Step 4 – Securing Acquisition Financing

Financing must be secured to fund the acquisition of the assets and business. Specialist lenders can provide facilities such as factoring, asset-based lending, and loans. Detailed plans and forecasts are required by all funders to justify valuations and assess the possibility of loss, ensuring security requirements are met.

Step 5 – Execution of the Pre-Pack Sale

After securing finance and satisfying compliance requirements, the proposed administrator is formally appointed. Following confirmation from floating charge holders, the administrator makes an application to Court. The business is sold to the ‘newco’ or a third party almost immediately thereafter, ensuring the process is rapid and continuity is maintained.

Advantages and Disadvantages of Pre-Pack Administration

Advantages

- Continuity: The procedure enables a ‘going concern’ sale with minimal interruption to ongoing business operations.

- Value Preservation: Assets such as goodwill, brand, and work in progress retain maximum value, which optimises the return to creditors.

- Cost Efficiency: The process contains costs by reducing the administrator’s time spent trading the company prior to the sale.

- Job Preservation: Retention of jobs within the new company is commonly secured.

Disadvantages

- Reputational Damage: The process may lead to reputational damage due to perceived non-transparency, particularly regarding the write-off of old company debts.

- Jobs cannot be shed in the process: This is due to the rules concerning TUPE see link opposite. So, it is not an effective rescue plan if overstaffing is one of the company’s main problems.

- Funding Challenges: The new company may face difficulties securing credit and must be able to fund the acquisition without undue reliance on immediate external financing.

- Market Risk: The requirement to market the business means the original owners may be outbid if they intend to purchase the assets back.

Costs

Given the complexity and requirement for legal input, a budget of at least £25k should be allocated for a pre-pack administration. If you require further advice on the suitability and process of a pre-pack administration for your business, you are encouraged to contact our experts for a detailed consultation.